We know, we know. Checks are old news. With the rise of digital payment platforms and automatic bill drafting, the average person’s need for checks has dramatically decreased in recent years. However, three out of four US consumers still keep checks on hand. Why?

There are many situations in which checks are necessary, particularly for making larger purchases or transactions. Whether you’re making a tuition installment, a down payment on a car, or sending in owed taxes, checks are typically the most common, if not required, method of payment. This is because it’s considered a more secure option than a digital alternative and can be just as convenient since recipients can use mobile check deposit features to access the funds.

So, if you’ve never handled checks before, it may be useful to know the basics about reading and writing them. You never know when this information will come in handy!

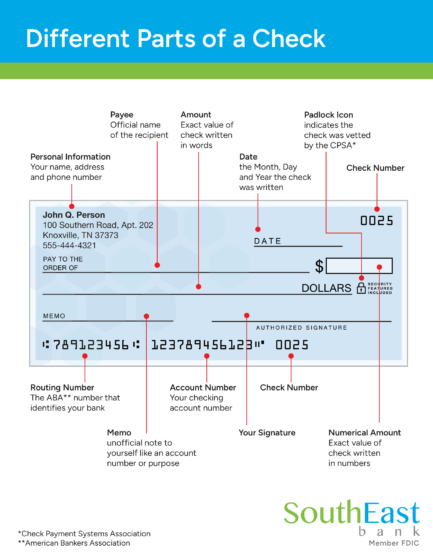

A Sample Check

Writing a check may seem like a simple task, but it’s important to do it correctly to avoid any issues. Be sure to follow these steps every time:

- Start by writing the date on the line provided. Use the standard format: month, day, and year.

- In the “Pay to the Order of” line, write the name of the person or business you are paying.

- Write the payment amount in numbers in the box provided. Be sure to include the cents as a fraction of 100 (e.g., $50.75), even if it is rounded to the dollar (e.g, $25.00).

- Write the payment amount in words (e.g., Thirteen hundred dollars and fifty cents) on the line below the recipient’s name. Make sure to write clearly and legibly.

- Sign the check in the bottom right corner using your legal signature.

- Finally, fill out the memo line if needed. This is optional and can be used to provide additional information about the payment.

The next step is important but happens in your checkbook rather than the check itself. Most checkbooks will come with a register, where you can keep a record of the check number, date, amount, purpose/memo, and payee of each check. This tool was vital when paper documentation was the only paper trail customers could maintain for their transactions between bank visits or statements. It remains valuable if only to keep track of the checks you’ve written. Once processed, the check should also appear on your bank statement.

Are Checks Safe?

When handled responsibly, checks are a secure method of payment because the recipient must match the payee of the check in order to deposit it. However, all forms of payment carry some level of risk. Here are some general safety tips to keep in mind:

- Keep your checks in a secure location, such as a locked drawer or safe.

- Avoid writing checks to unfamiliar individuals or businesses.

- Never leave blank spaces on your checks. Fill in all fields to prevent unauthorized alterations.

- Use black gel ink pens when writing checks, since this type of ink is harder to tamper with.

- Regularly reconcile your bank statements to ensure all transactions are accurate.

- When mailing a check, post it directly from the postal service in order to minimize the potential for theft.

As with your debit card or digital payment account, it’s important to stay vigilant and take precautions to protect your financial information when using a check.

Final Considerations

There are both pros and cons to keeping and using checks as a form of payment. Some banks charge for the use of checks, yet they provide a convenient, flexible way to give gifts in the case of holidays, weddings, or other special occasions. Recipients without bank accounts may have to pay a fee in order to cash a check, but for the writer there is proof of payment which can provide some peace of mind.

For anyone with a checking account, it’s helpful to know how checks work, when they can come in handy, and how to safely write and manage your checks. For any additional questions you may have, we encourage you to visit your local SouthEast Bank branch where our team would be happy to assist you.