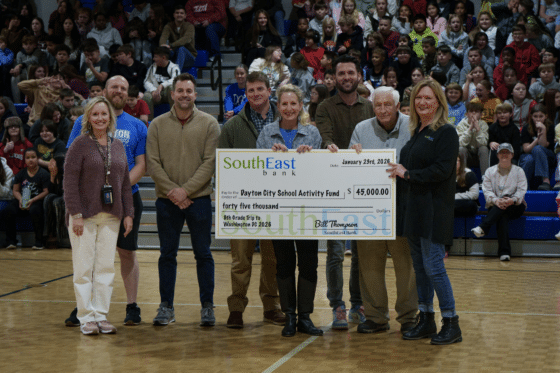

In March 2026, with the help of a $45,000 donation from SouthEast Bank, Dayton City School (DCS) students and chaperones embarked on the annual 8th grade field trip to Washington, D.C. In addition to the educational opportunities this trip offered — including visiting federal landmarks, museums, and memorials — for students like Riley Gann it was a “once in a lifetime thing.”

“It was also my first time ever out of the state of Tennessee,” said Gann.

“A trip like this is an investment in the future citizens of our government,” said Candice Tilley, 8th grade history teacher at DCS. “It’s an unforgettable way to better understand that role.”

For five years, COVID-related closures and rising costs made this U.S. Capitol trip untenable, but in 2024 SouthEast Bank stepped in to provide a donation that would make the cost less prohibitive to Dayton City Schools and its students. Now, after a similar donation in 2025 and again in 2026, this local partnership has become another element of the annual tradition.

“SouthEast Bank’s commitment to investing back into our communities starts with education,” said Jimmy Dalton, Community Reinvestment Officer at SouthEast Bank. “We know that experiences like this not only teach but also inspire a deeper sense of history and belonging, the impact of which can be far-reaching. We’re proud to say this is our third year partnering with Dayton City Schools to provide this opportunity.”

This was such a memorable and fun adventure with my friends. I really appreciate SouthEast Bank for sponsoring this trip and I hope they’ll continue for future grades.”

DCS Student Maggie Ni

When asked about their favorite memory from the field trip, students commented on the historical markers that impacted them, as well as the social and cultural aspects that stood out in their experience.

“My favorite thing was going to Ford’s Theatre,” said DCS 8th grader Ryleigh Pearson. “This trip meant a lot to me because I get to learn about where I come from and I can appreciate what I have as well as the people that fought for what I have.”

“My favorite thing was the Lincoln Memorial. I also liked the museum about world history and the food,” said William Garcia. “This trip meant a lot to me as a Mexican-American.”

“My favorite parts of the trip included the 9/11 Memorial, the Natural History Museum, and the Air Force Memorial,” said Caitlyn Bowman. “The hotel, restaurants, etc. was beyond what I imagined they’d be like. Definitely my favorite school trip ever.”

“I liked the Korean War Memorial because you could see people’s faces on the wall,” said Tripp Soyster. “I also liked the Capitol Building because you could see the people that run our country at work.”

“My favorite part of the D.C. trip were the national museums, the JFK Center for the Performing Arts, and the gorgeous buildings and memorials in Washington,” said Maggie Ni. “This was such a memorable and fun adventure with my friends. I really appreciate SouthEast Bank for sponsoring this trip and I hope they’ll continue for future grades.”